Blue Bottle Coffee: The Analytics Behind the Leading Specialty Coffee Chain

Blue Bottle Coffee: The Analytics Behind the Leading Specialty Coffee Chain

Why does Starbucks have 16,000+ US locations, Dunkin nearly 10,000, but the leading specialty coffee chain has less than 100?

Hi all - it’s Jordan here from The Analytics Behind. We break down brands, industries, and business topics with a business analytics lens - a blend of strategy & analytics. If you enjoy our work, we’d love for you to subscribe to get our content directly to your inbox.

One of life’s small joys for me is good (cold brew) coffee.

The market for away-from-home coffee is large and filled with well-known brands like Starbucks and Dunkin. These brands, while ubiquitous, are not specialty coffee brands - they’re mass market.

Local, independent shops serving specialty coffee are also common - you’ll find many scattered throughout midsize and larger cities.

Less common are brands that (1) serve specialty grade coffee and (2) are on a nationwide scale. Among the largest is Blue Bottle Coffee - owned by Nestle.

Why aren’t there more nationwide specialty coffee brands? Why can there be ~16,000 Starbucks in the US, 9,600 Dunkin, and only 76 Blue Bottle locations?

This week we’re breaking down the coffee industry, Blue Bottle’s positioning & niche within the market, and the growth opportunities & constraints associated with that positioning.

THE COFFEE MARKET SEGMENTATION

Let’s start simple.

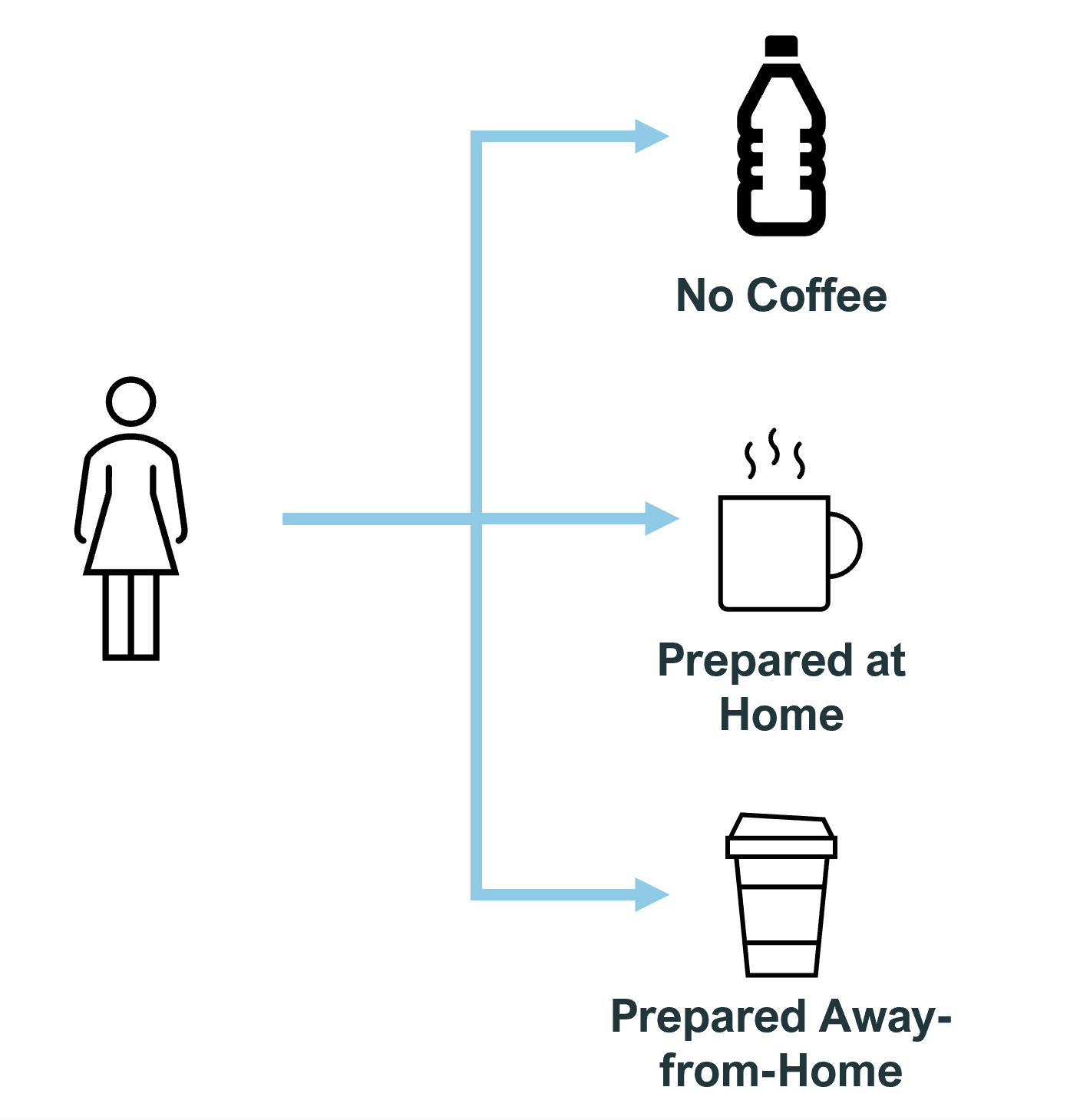

Consider three scenarios someone that wakes up in the morning. The person:

Does not drink coffee

Drinks coffee prepared at home

Drinks coffee away from home

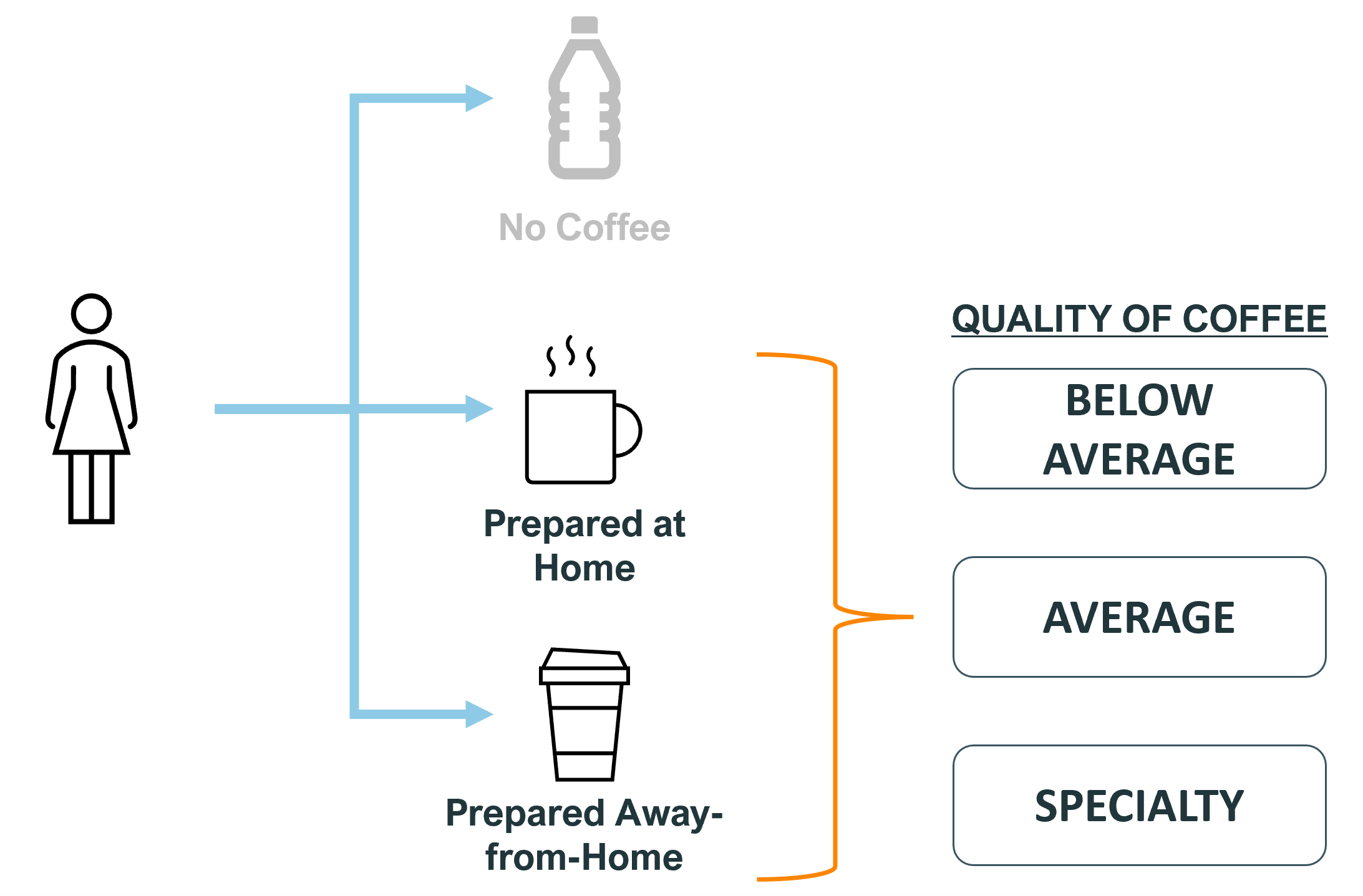

Coffee drinkers, both at home and away-from-home, then have a choice - how much do they value the grade (quality) of the coffee?

Coffee brands decide which of these segments they want to compete in.

Do they want to be mass market and more affordable, high-end and expensive, or somewhere in-between? Do they want to operate cafes or simply sell beans for consumers to make at home?

The choices come with tradeoffs.

A café is expensive to run but generates better brand visibility and captures the prepared-away-from-home drinkers. Specialty coffee brings in higher revenue per cup, but has a smaller addressable market.

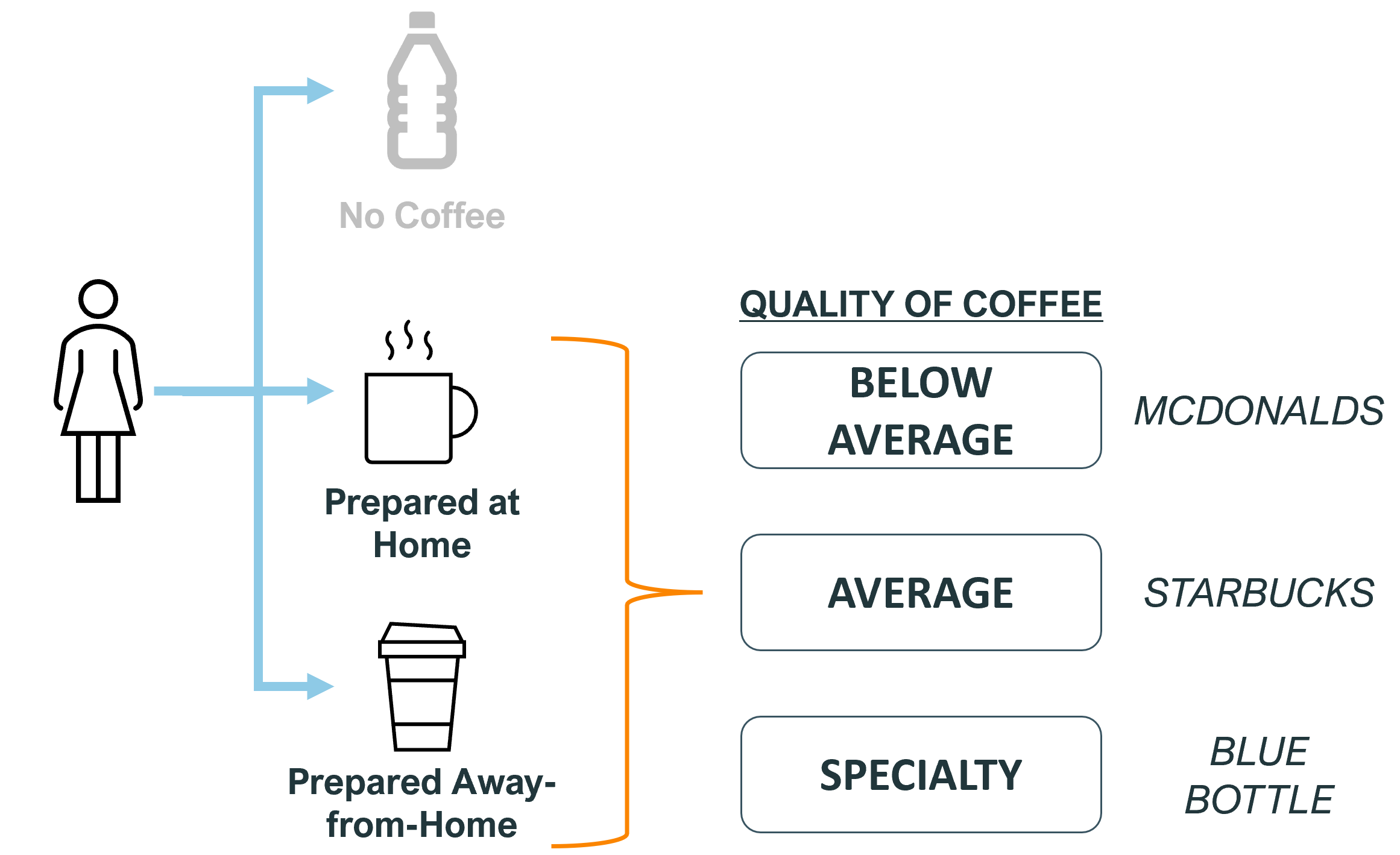

The framework serves as the backdrop for the industry and how to think about competitive positioning & opportunity - Dunkin & McDonalds are affordable, Starbucks is an affordable luxury, and Blue Bottle is a luxury.

How does a company’s segmentation affect their market planning, growth opportunities, and growth constraints?

PREMIUM MARKET POSITIONING

Knowing that Blue Bottle competes in the specialty segment and sells to both the at-home and away-from-home consumer, what do they need in an area to succeed?

The obvious answer is income - they need to be in areas where high earners live, work, or spend time.

To build on this, they need to be in areas where a lot of high earners spend time. A coffee shop needs sufficient volume to thrive, even at $5-$6+ per coffee.

Opportunity for a premium coffee brand sits at the intersection of wealth and daytime population density (residents, workers, leisure).

Another challenge of a coffee shop is that their day is effectively cut in half from a revenue perspective. Visitation to coffee shops peaks in the morning and tapers off the rest of the day.

Thus, a premium coffee brand needs to be in places where there are high earners and high density and where these people spend time in the morning.

Now consider when an area is primarily commercial (office space), we only have 5 core selling days instead of 7. In this scenario, the company needs to make 7 days worth of revenue in 5 (half) days.

Every constraint shrinks the market further. A specialty brand has limited options that meet the minimum market size, income, people flow, and area characteristics.

Contrast this to Dunkin, a more affordable option. The areas that are addressable to a Dunkin franchisee are much wider - almost anywhere with regular flow of people like shopping centers or busy roads.

This is why Dunkin has almost 10,000 US locations and Starbucks has over 16,000, but Blue Bottle - the leading specialty chain - has only 76.

The available areas and locations that can sustain a mass market coffee brand far outweigh the number of places that can support a specialty coffee brand.

BLUE BOTTLE’S MARKET PLANNING & GROWTH OPPORTUNITY

To recap, Blue Bottle competes in the premium segment of the market and as such needs to be near people that (1) value specialty-grade coffee and (2) have the means and desire to pay for it.

This limits their pool of available markets to large urban environments with high-income earners, specifically the areas where these high-earners live and/or work.

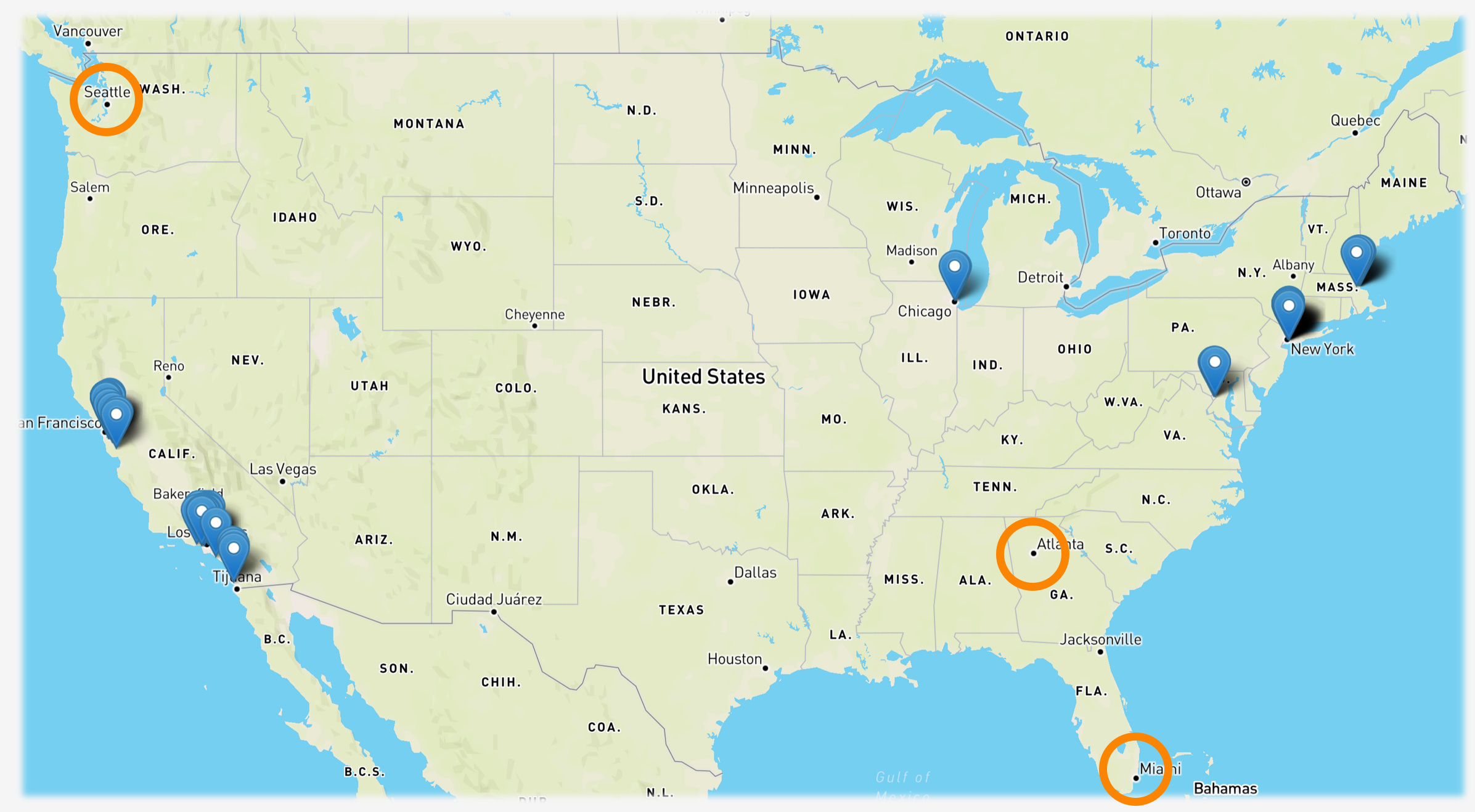

The list of markets where Blue Bottle operates is not long - just 6 - though spans coast-to-coast.

Blue Bottle locates in dense urban areas and bustling, upscale communities near urban cores. These are areas with high employment, population density, and income.

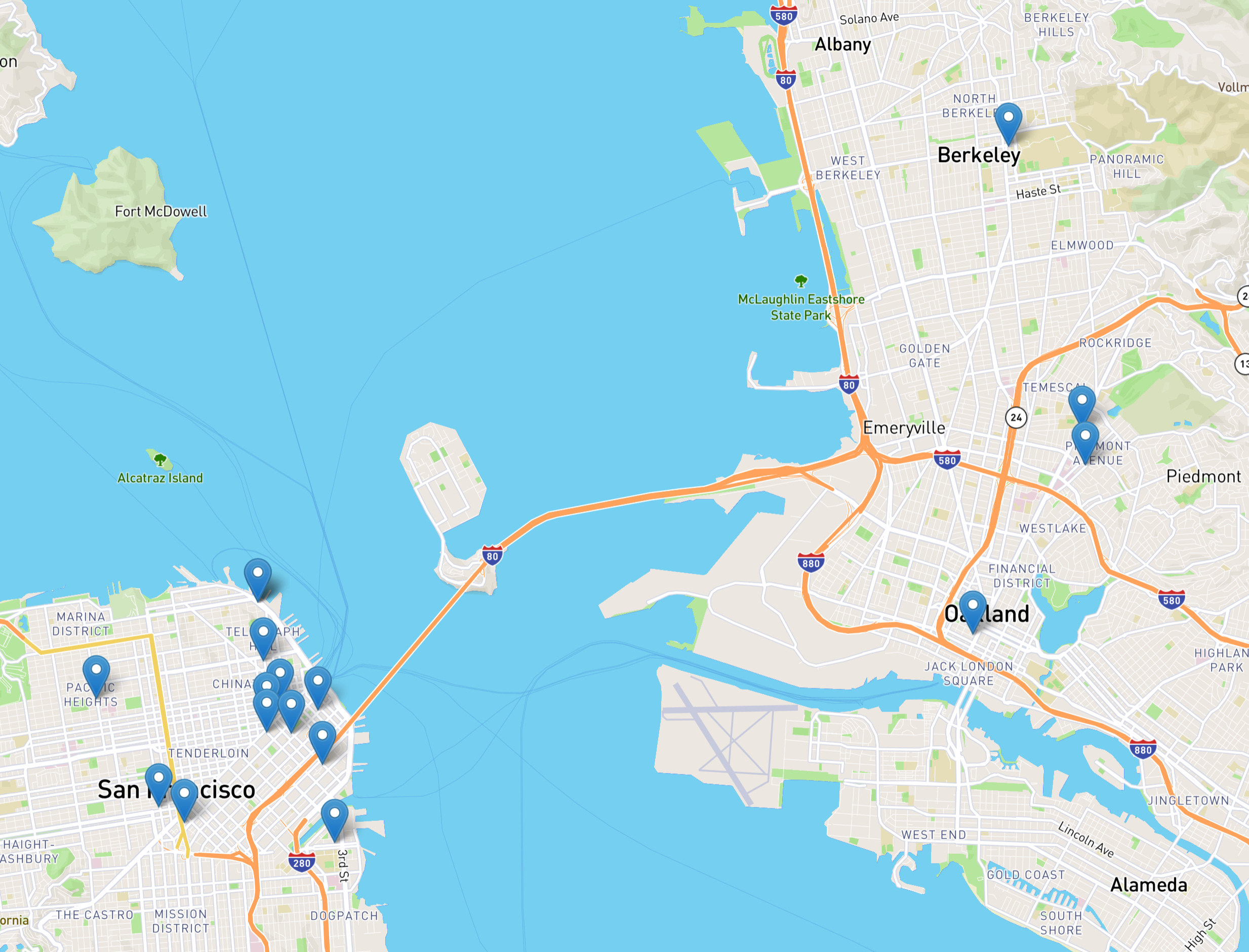

Consider the locations in the San Francisco-Oakland-Berkeley metro. There are 12 locations in downtown San Francisco, 3 in Oakland, and 1 in Berkeley.

The locations in downtown are generally near areas that (before COVID) were bustling urban hubs. The location in Berkeley sits just off the campus of UC Berkeley.

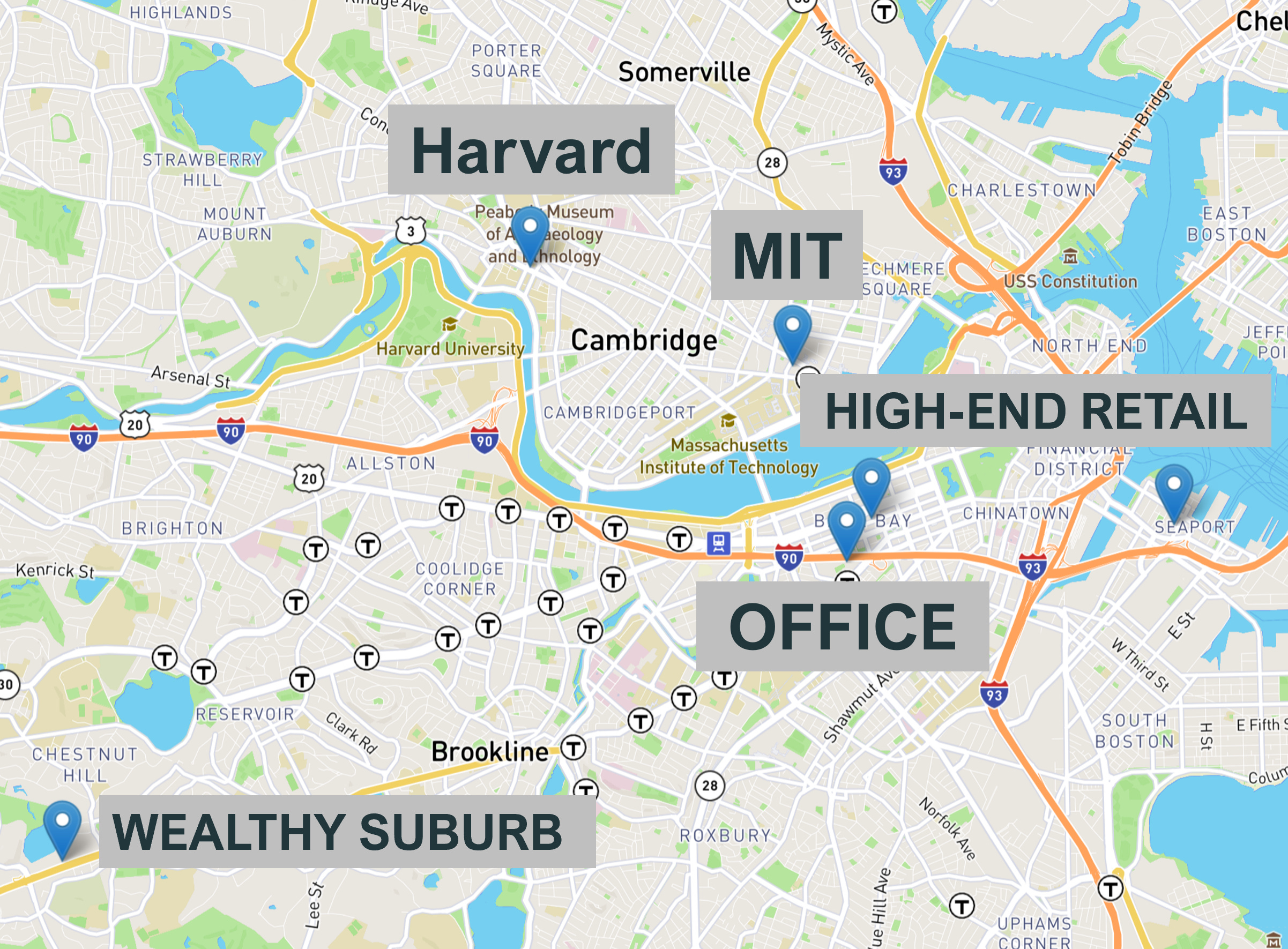

Let’s switch over to Boston, where there are 6 locations.

These locations are interspersed among top tier universities, high end retail districts, concentrations of white collar jobs, and wealthy suburbs.

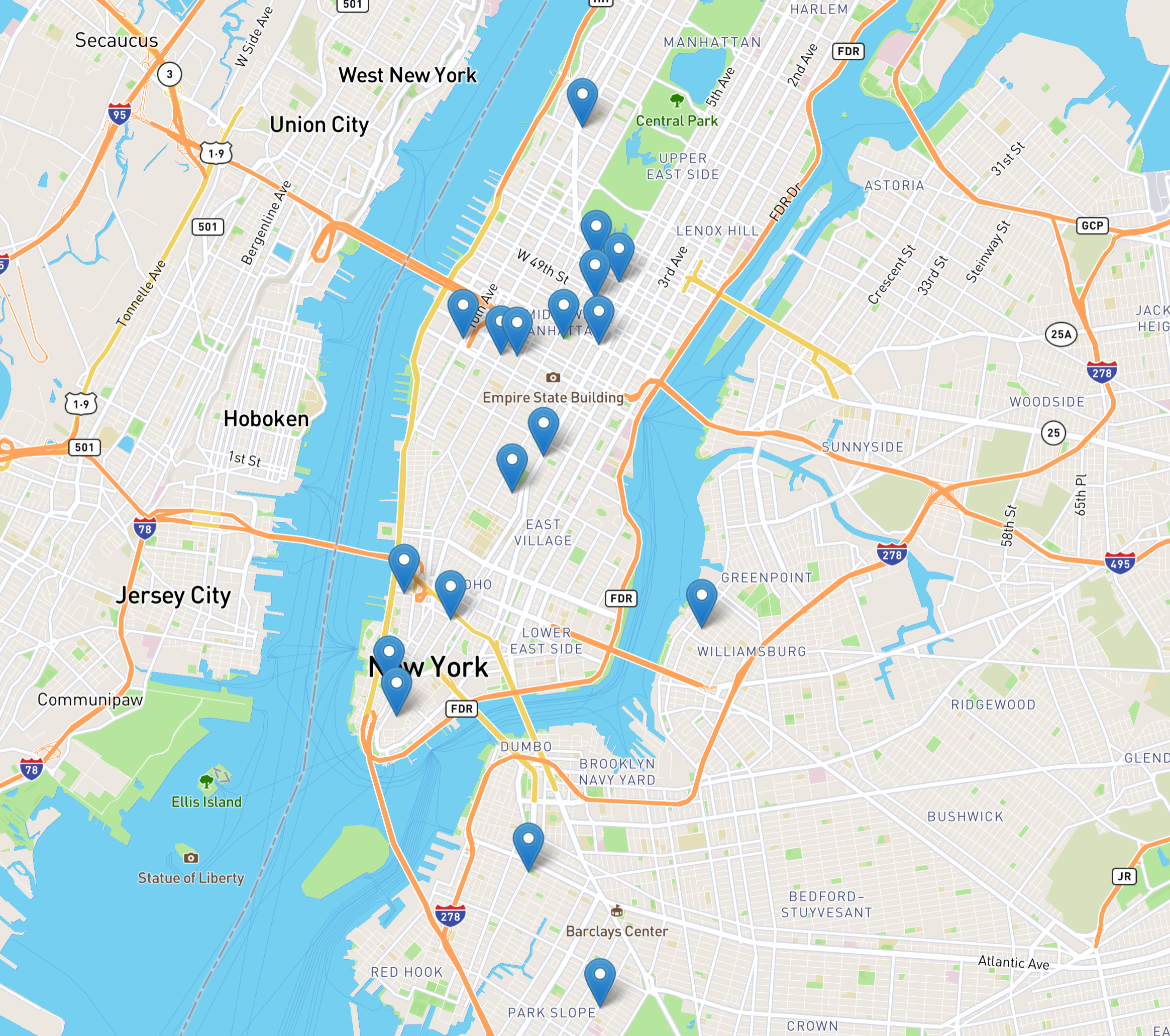

Similar patterns play out in New York where the brand has built density in Manhattan’s bustling office & residential areas with select locations throughout Brooklyn.

Notice the pattern in the markets and places in those markets that Blue Bottle locates? This concept only works in the largest, densest, wealthiest areas.

When the area is right, Blue Bottle can densify the market - some NYC locations are just blocks from each other - but there aren’t many “right” areas.

Blue Bottle’s growth opportunity will always be limited by the markets and areas that meet their minimum requirements to succeed, similar to a brand like sweetgreen, but that doesn’t stop it from developing profitable stores in those targeted areas.

As an example of the magnitude of the growth limitations, Starbucks has ~250 locations in New York City & Brooklyn compared to Blue Bottle’s 19.

So, knowing the target market and constraints, is there anywhere left that the company can grow? The answer is likely yes.

There are still new market opportunities for the brand to grow, but not many. Based on their current footprint & target customer, I’d say the most likely new markets that have high potential for the brand are Miami, Atlanta, and Seattle.

These are metros that have concentrations of wealth, mixed urban environments, large addressable markets, and established specialty coffee scenes.

In existing markets, the footprint is still light in Washington DC and Chicago relative to their opportunity, likely leaving room for more existing market growth too.

FINAL THOUGHTS

The coffee market operates just as many other markets do - identifiable segments, competitors that fill different segments, and an opportunity to build a brand around a distinct value proposition.

Blue Bottle is one of the few that has applied a nationwide growth strategy within the specialty segment of the market, benefiting from a higher spending customer base while also being limited by the available growth opportunities.

The more targeted the value proposition, the more important it becomes to align the market planning with the value proposition. Dunkin can work just about anywhere, but specialty brands find more limited - but lucrative - growth opportunities.

Like what you read? Subscribe to get our content directly to your inbox.